Special Offers

Special Offers

Car leasing deals from the experts

Know exactly what you are looking for?

Use our Advanced Search

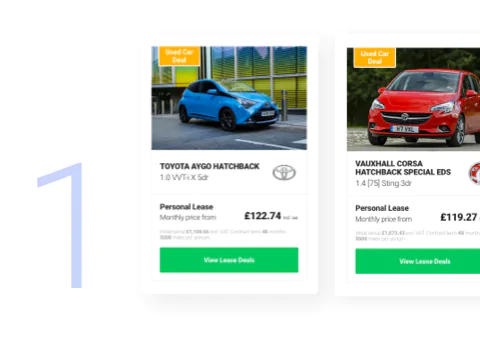

Our hottest special offers.

See all special offers

Automatic

Automatic  0-62 MPH in 6.6s

0-62 MPH in 6.6s

Petrol

Petrol

176.6 MPG

176.6 MPG

Most Popular Brands.

See all popular brandsTrusted by customers nationwide.

The easy way to lease your dream car!

-

Find your dream car

Browse thousands of new and used vehicles on Hippo Leasing to find your dream car! Can't find what you're looking for? Then just give us a call.

-

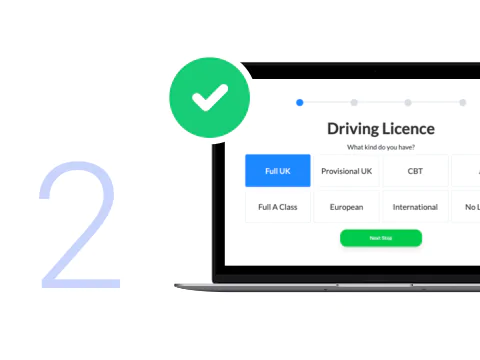

Get pre-approved

Speed up your application and get preapproved by using our FREE soft credit check (with no impact on your credit score*).

-

Reserve your car online

Once you're approved you'll be able to view more cars, and even reserve your dream car online, using your MyHippo account.

-

Start driving

Either pick up your new vehicle from our Blackburn showroom or have your car delivered to any location in the UK.

No jargon, just hassle free buying.

How it works

Deals on new & used cars

Deciding whether to go new or used can be tricky when you’re trying to lease a car - which is why we offer both options. We also offer personal and business lease vehicles!

Free impartial advice

We train our account managers to get the best deal for you - we won't try to upsell you a Lamborghini when you're after a Polo! We put you at the centre of the process, not selling a car or maximising a lease agreement.

We’ll arrange everything

From initial contact we take care of everything! From finding your dream vehicle to arranging collection or delivery. You’re in safe hands with Hippo.

Apply now, get a

decision in minutes.

The fastest way to check whether you'll be pre-approved for car finance with one of our top-tier or specialist lenders. A short finance application that won’t affect your credit score or appear on your credit profile.

Speed up your car leasing journey

Speed up your car leasing journey- Find out within 60 minutes if you'll be pre-approved by one of our lenders

- Initial application doesn't affect your credit score

- Results sent directly to your email

Speed up your car leasing journey

Speed up your car leasing journey

Frequently asked questions.

Help DeskWhat is car leasing?

Car leasing is an easy way to rent a vehicle over a set time period with one, affordable monthly payment. We have various lease contracts available, which you can choose depending on your requirements; and we also offer leases for personal and business use. When your contract is complete, you can return the vehicle and lease another one.

How does car leasing with Hippo work?

Leasing a vehicle with Hippo is quick and easy. Follow our simple four-step process to get your car:

1) Apply for finance for leasing; our soft credit check has no impact on your credit score.

2) Find the vehicle you love and submit your full application with your trusted account manager.

3) Arrange to collect your car from our Covid-safe showroom or arrange to have your car delivered anywhere in the UK.

4) Drive your car and return it when your lease agreement ends!

Do you require a credit check to get accepted for finance?

Yes, you’ll have to go through a credit check, but you can discover whether you’re likely to be accepted for a lease deal with our FREE soft credit check that has no impact on your credit score. If approved, we can start your application, where you’ll go through a hard credit check.

Do you take part exchange?

Yes. If you’ve got a car to part exchange, you can use it as a contribution to your new lease deal. Its value can either go towards a deposit on your new vehicle, which could lower your monthly payment, or towards paying off any outstanding finance on your current car.

Do you include insurance with your deals?

No, we don’t include insurance in your car leasing payment. You’ll have to arrange your insurance before you drive the vehicle.