Special Offers

Special Offers

21st October 2016

21st October 2016  10 min read

10 min read When running a business that requires vans for the job, the decision on where to acquire them from can be difficult. What is the best, most efficient and the cheapest way of getting maybe just one van or a fleet of vans?

As a sole trader, small business or fleet manager of a large fleet of company vehicles, you may have considered hiring or even buying vans. However, van leasing has recently become a very popular choice, due to the many benefits of van lease deals. But, is leasing your van or commercial vehicle the best option for you? We’ve weighed up the pros and cons of van leasing to help you choose the best way to acquire your new van.

What is van leasing?

Van leasing, otherwise called contract hire, is an agreement for a set period of time, typically 24-60 months, whereby you make pre-agreed monthly payments. A deposit may be required at the start of the agreement although, there are now many new and used van deals available that don’t require a deposit – with Hippo Leasing we are happy to help with whatever requirements you have.

Deal Analyst and New Car Specialist, as well resident leasing expert at Hippo Leasing, Matthew Bailey explained the difference: “Leasing a van differs from buying the van, either with cash outright or through hire purchase, as you do not own the van. A middle option is the PCP agreement, where you have the option to buy the vehicle through a balloon payment or to hand it back or upgrade. Lease purchase is another middle option of financing a van in order to own it.”

However, a business – be it a tradesman or SME – will not always have the liquidity to buy a new van in cash, and it usually makes sense to acquire a commercial vehicle through finance.

That’s why Hippo has created a handy infographic to highlight the benefits and downsides of leasing your van.

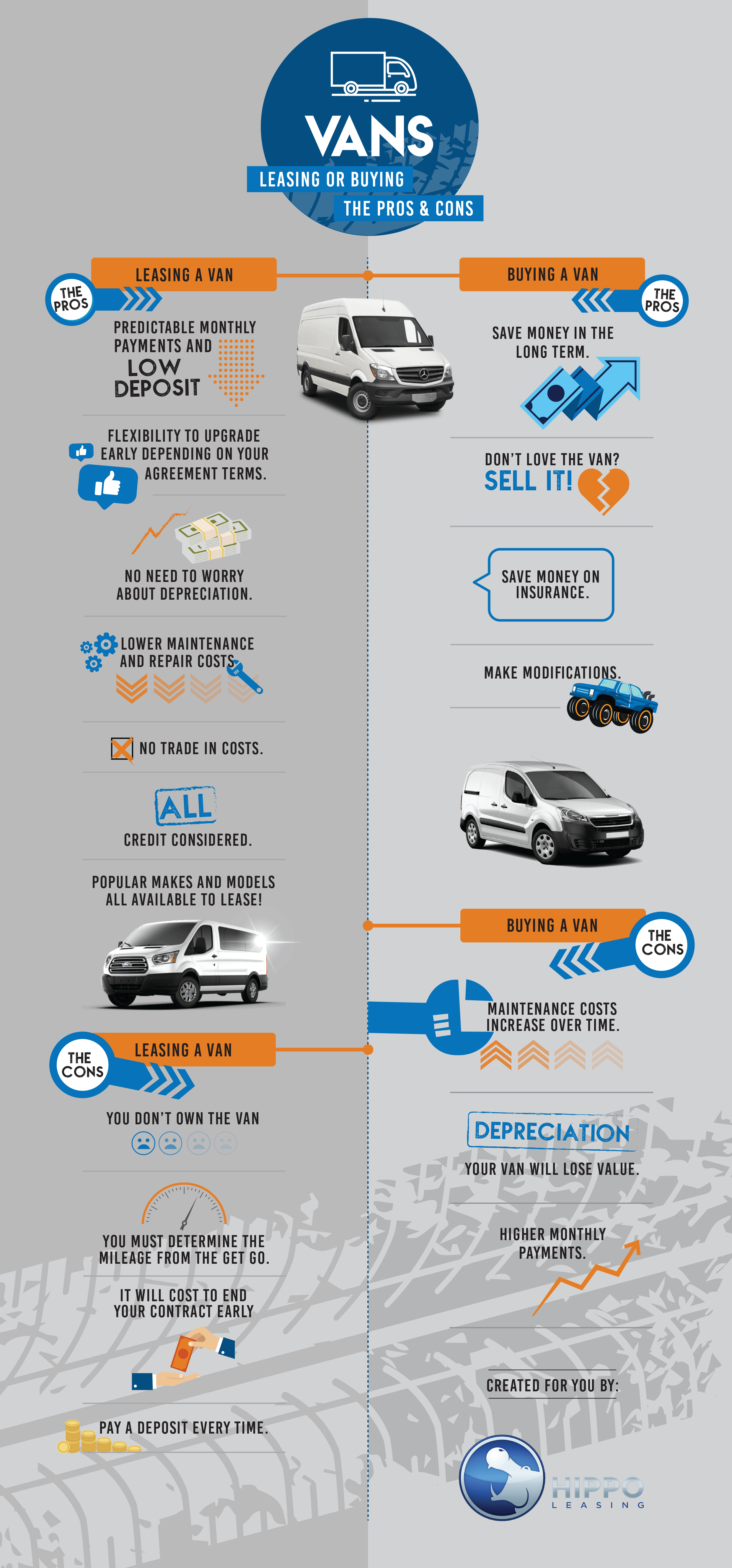

Pros and cons of van leasing

As you can see, there are several excellent benefits to consider when it comes to leasing, and we explain them to you below.

Why should I lease a car?

1. Predictable monthly costs and low deposit

When taking a lease agreement out on a van, you will have fixed, predictable monthly costs over your agreed leasing period, as well as having a low or maybe even no deposit.

2. Flexibility to upgrade early, depending on the agreement terms

Upgrading your van brings a business a cleaner, more-cost-effective fleet. If you are interested in upgrading your vans or the agreement itself, there is flexibility regarding updating your vans depending upon what has been agreed in the agreement terms.

Matthew added: “Being committed to a van because you own it means upgrading to a cleaner, cheaper to run vehicle becomes difficult due to the value gap between your current van and your desired van. With leasing, this isn’t a problem.”

3. No need to worry about depreciation

A leasing contract means that if you don’t wish to deal with the vehicle’s depreciation and subsequent selling of your vans, then you can simply hand them back.

4. Lower maintenance and repair costs

There are lower maintenance and repair costs for your vans when you lease them.

5. No trade-in hassle

You don’t have to be concerned about trading the vans in, you can simply hand them back to your leasing company.

6. All credit considered

No matter if you have excellent credit or poor credit when it comes to van leasing, all credit is considered.

Matthew weighed in, noting: “For tradesmen and businesses, having access to a van is fundamental to their livelihood, and often this is a limitation when it comes to buying a van, that is less of a problem for leasing. A credit score shouldn’t be so limiting when they are looking to either acquire a van for the first time or for expanding their fleet to fulfil their growing business, that’s why Hippo Leasing believes that offering vans to low credit customers is an essential service.”

7. Popular makes and models, all available to lease

With van leasing, you can get new makes and models as well as the already popular models.

Matthew explained further: “Paying off the depreciation as opposed to the van’s value ensures lowers the monthly payment so that that newer and more popular vans are more accessible to more budgets – this is great for fleets as these higher quality vehicles can provide greater value to a business.”

8. Tax-deductible

When leasing a van for business, you can claim VAT back.

Bailey commented on why businesses should love this benefit: “Leasing has a huge bonus over buying – in that it is tax-deductible. This is the same for any form of renting over buying outright for businesses, and means for commercial customers, the tax saving provides a significant saving.”

Cons of van leasing

1. You won’t own the van

If you find you very much like your vans and are keen on owning them, unfortunately, you only have that option if you take out a personal contract purchase agreement (PCP).

Matthew remarked: “It’s well-known that leasing your vehicles is best-suited to those who regularly update their fleets. If you find your current van super reliable that you want to keep it past the contract period, then sadly this isn’t an option with contract hire. You will need to take a PCP, HP or LP contract for a similar van – things that Hippo can help you with when the time comes.”

2. You must determine your mileage from the get-go

If you are taking out one van or a fleet of vans, you must still determine the mileage for each van from the start of the contract hire agreement, and this can be a downside for those who don’t want limitations in how far they can drive.

“This is a huge part of your lease agreement – you need to know how much you expect your vans to be driven each year, as this affects the vehicle’s value at the end of the contract, and will influence monthly payments. A van that drives less also depreciates less and therefore will benefit from lower monthly payments. At the same time, exceeding your mileage will be subject to a per mile fee at the end of the contract,” Matthew said.

3. It will cost you to terminate a vehicle contract early

If you find that you want to terminate your van leasing agreement instead of upgrading it, there will be a cost for early termination of the contract.

4. Pay a deposit every time

If you are leasing with a deposit, you need to pay for a deposit every time you upgrade. If you are opting for a no-deposit lease, however, this is not an issue.

Matthew added: “An initial payment helps to bring your monthly payments down, and how much you put down is up to you. However, customers who plan on paying a downpayment will need to do so each time they lease, so this needs to be accounted for. Of course, at Hippo we’re finding no-deposit contract hire is a popular alternative as it removes the need for a deposit.”

Should I buy a van instead?

Buying a van involves any method of paying for the value of the vehicle – whether you want to buy a van outright, hire purchase, PCP or lease purchase. For those that aren’t entirely sure whether a lease is the best solution to acquire a new van for their fleet, buying offers its own boons that ought to be considered:

Benefits of buying a van

1. Save money in the long-term

Once you’ve paid off the van, you only need to worry about paying for maintenance and running costs, thereby saving in the long run.

Matthew explained why van buyers are attracted to owning their van: “A reliable van is a van that requires little maintenance after it has racked up miles, and this will ultimately save owners hundreds of pounds a year if the vehicle requires no major fixes or part replacements.

“Additionally, owning the van saves on monthly payments, but the fleet manager will need to know that the yearly cost of maintaining a fleet of vans a business owns is lower than the cost of leasing vans, and as vans age, the maintenance cost rises,” he noted.

2. Don’t love the van? Sell it!

When you own the van, you are free to sell it and recoup part of your investment (remember, cars depreciate) and put it towards your next van. If you have any outstanding finance, this must be settled first.

“Selling the van is probably the biggest benefit of owning a van. Any funds you have saved up can go towards upgrading to a better van, although it bears repeating that if the van is old, it will have lost value to the point where a new van is out of reach, and a business is losing out on acquiring more reliable, greener and money-saving vans,” commented Bailey.

3. Save money on insurance

When you own the car, your insurance drops with the value of the car, translating into lower insurance payments for you.

4. Make modifications

When the vehicle is yours – it’s your to do what you please with.

Downsides of buying a van

1. Maintenance costs increase over time

As wear-and-tear takes its toll on the van, it will cost you money to repair the van. Be sure the maintenance doesn’t exceed the van’s vehicle.

Providing extra insight to this, Matthew said: “Your van will cost money to fix and replace parts as it ages, and so long as you take care of the vehicle, you should see a great return of mileage from any van over time. However, for older vans, maintaining them to level where they provide your business value can add up, and due to losing value, selling the vehicle may not yield a significant return.”

2. Depreciation

The big ‘D’ word in the car world can’t be avoided. Vehicle’s lose value, making it harder to upgrade when the car is no longer worth keeping.

3. Higher monthly payments

When paying off the value of a van, this translates to higher monthly payments, and can also limit the number of vans available to you, depending on your budget.

“Over a typical lease contract of three years, you can expect the van to lose around half its value – this translates to lower monthly payments than you would expect when it comes to paying off the car in the same period,” explained Matthew.

Matthew summed up the two options for those seeking a new van: “Ultimately, how you finance your van depends on your personal preferences. Leasing a van provides convenience and peace of mind that you don’t need to worry about things going wrong with your leased van, with the main downside that the van will not be an asset that can return some of its value to you should you need it.

“An owned van makes financial sense if you intend to keep it longer than it takes to pay it off, and providing maintenance does not become excessive, you may even save money over time.”

Hippo Leasing has a large range of vans and we can offer customers great van leasing deals for business and personal use, and if buying a van is your preference, all our vehicles are available for sale – simply speak to our sales team to find out more.

To find out more about leasing commercial vehicles with Hippo, simply, drop us an email at info@hippomotorgroup.co.uk or give us a call on 01254 956 666. Alternatively, enquire here by filling in a short enquiry form.