Special Offers

Special Offers

How it works

Leasing a car doesn't have to be a lengthy, drawn-out procedure. Simply follow our 4 step process and you'll be driving in a jiffy!

-

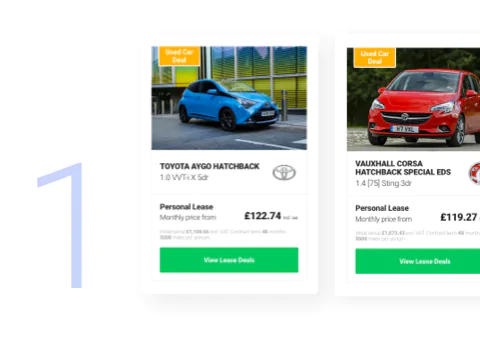

Find your dream car

Browse thousands of new and used vehicles on Hippo Leasing to find your dream car! Can't find what you're looking for? Then just give us a call.

-

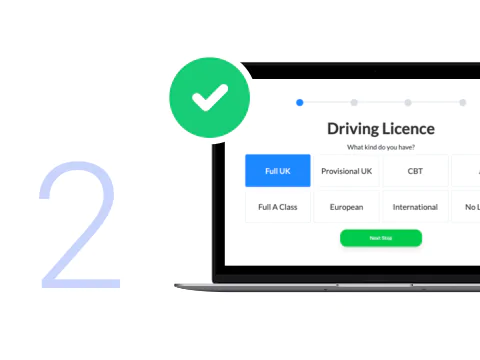

Get a decison

Speed up your application and get a decision by using our FREE soft credit check (with no impact on your credit score*).

-

Reserve your car online

Browse thousands of new and used vehicles on Hippo Leasing to find your dream car! Can't find what you're looking for? Then just give us a call.

-

Start driving

Either pick up your new vehicle from one of our showrooms or have your car delivered to your home.

It only takes a minute ⏱️

Speed up the process of your car leasing journey and check your eligibility - with no impact on your credit score!*

*Rates from 12.9% APR. Representative APR 13.9%. We are a credit broker, not a lender.

Get a car that suits your lifestyle

We stock a massive selection of cars from the best manufacturers in the world; you’ll find the electric innovation of Tesla and the excitement of BMW in our car range.

We also stock cars of various body types and styles, so whether you’re looking for something that's city-slick and trendy, or something rugged and country road-ready, we’ll find a car to suit your lifestyle. Browse our huge selection of vehicles.

Use Hippo to weigh up your options

Use our site to compare personal and business lease deals, no deposit, bad credit, and special offers. We use a panel of lenders, so you know you’re always getting the cheapest deal from the best lender. You can also compare different types of lease contracts; we’ll give you free, impartial advice. We are a credit broker, not a lender.

We inspect and test used vehicles before your lease

When you’re leasing a used car, you want to know you’re getting it in the best possible condition.

That’s why we check all our vehicles using the Hippo 130-point check, which is carried out by our manufacturer-trained car technicians.

And if a vehicle doesn’t pass the test, it doesn’t leave our garage. We’re committed to providing quality cars, so we give you a 3-month warranty for complete peace of mind.

Get bolt-ons for extra security

If you want even more protection during your lease contract, get complete peace of mind with bolt-ons like added maintenance, gap insurance, paint protection and an extended warranty.

Speak to your account manager to discuss any additions and be sure to browse our bolt-ons to see if any appeal to you.

We offer collection and delivery options

When your application is finalised, and you’ve been accepted, you can either collect your car from our Blackburn-based showroom, or we’ll deliver it anywhere in the UK!

Plus, both our delivery and collection methods follow government social distancing guidelines, and we sanitise all our vehicles before they leave our showroom.

Check your eligibility in minutes!

If you want to speed up your application you can use our FREE soft credit check to determine whether you’re preapproved for finance. Plus, it won’t have an impact on your credit score.

Begin your car leasing journey with Hippo and apply today! We’ll be in touch to discuss your application further, so you can sit back, relax and find your dream car.

Our online preapproval application:

Is quicker than applying over the phone

Is quicker than applying over the phone- Isn’t visible to lenders and won’t appear on your credit file

- Sends your results directly to your email within 60 minutes

Is quicker than applying over the phone

Is quicker than applying over the phoneWe’re always here when you need us

Whether you’re partway through your application or you want to make a simple enquiry, we’re always here to support you.

Our live chat is available on any page on our website; you can leave a query on our contact page or call us if you have an urgent message.

What happens after you apply?

If you've already chosen the car you want, a member of our team will be in touch with some more details and to confirm you're happy with the price. If you haven't, don’t worry. Our team can help you find the vehicle that's right for you.

It only takes a minute ⏱️

Speed up the process of your car leasing journey and check your eligibility - with no impact on your credit score!*

*Rates from 12.9% APR. Representative APR 13.9%. We are a credit broker, not a lender.